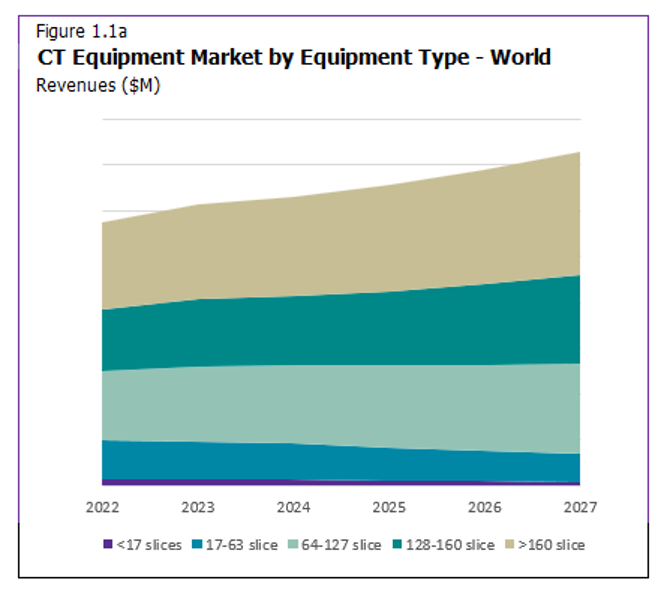

In 2024, the CT Equipment market faced tough conditions. China, a thermometer for global market growth, saw orders to relieve pent-up demand released late in the year as a trickle rather than a surge, whilst globally, prices remained high despite the easing of inflation. As a result, the CT Equipment market contracted in 2024, and the 2025 to 2029 revenue CAGR is forecast at mid-single digits. Uncertainty looms heavy over the CT equipment market, particularly in the US, as tariffs are expected to be enforced from mid-2025. These tariffs will no doubt impact pricing for imported systems and components and introduce concerns around the financial viability for smaller vendors in the market. Globally, the 128 to 160 slice segment and greater-than-160-slice segments are projected to grow fastest at mid- to high-single-digit revenue CAGRs from 2025 to 2029.

The advent of tariffs is growing increasingly prominent as time goes on, and while the situation

is still highly changeable, the likely impact is expected to be on pricing, supply chain disruption, competition and market access as well as regulatory and strategic compliance. Tariffs will raise the cost of imported components, leading to higher production and acquisition costs, and companies will begin diversifying or relocating supply chains to mitigate the impact, causing short-term complexity and disruption. Vendors may act cautiously, reassessing market access strategies and possibly delaying investment or shifting operations to maintain compliance and reduce costs under evolving trade regulations. The rising barrier to entry in the US market will likely limit activity from smaller vendors who are more risk-averse.

is still highly changeable, the likely impact is expected to be on pricing, supply chain disruption, competition and market access as well as regulatory and strategic compliance. Tariffs will raise the cost of imported components, leading to higher production and acquisition costs, and companies will begin diversifying or relocating supply chains to mitigate the impact, causing short-term complexity and disruption. Vendors may act cautiously, reassessing market access strategies and possibly delaying investment or shifting operations to maintain compliance and reduce costs under evolving trade regulations. The rising barrier to entry in the US market will likely limit activity from smaller vendors who are more risk-averse.

Clinical Drivers Impacting Hardware

Clinical needs are playing a growing role in the hardware advancements of CT equipment market, particularly in the key clinical areas including cardiology, neurology and oncology. The advent and expansion of lung cancer screening programmes throughout the EU is translating to a renewed focus on mobile CT solutions, with vendors releasing tailor-made mobile CT solutions to facilitate their use in screening high-risk populations. Mobile solutions have also been a key topic of interest for stroke applications with the introduction of Mobile Stroke Units (MSUs) by major vendors to capitalise on the pre-hospital imaging market. These solutions hope to improve patient outcomes by allowing for quicker response in the first critical hour following a stroke. Reimbursement is still variable for mobile solutions globally, which may limit adoption. The retrofit strategy many vendors have taken in making a traditional CT system as compact as possible, to fit into a large truck or ambulance, may further hamper the growth potential for mobile units due to the limitations of such large, mobile systems. These solutions leave little room for other uses, such as beginning treatment in the case of MSUs, or changing and waiting rooms for lung cancer screening, which provides some hope for the market to continue innovating in response.

Tangible Responses to Workforce Shortages

As concerns over radiologist shortages have continued to mount in the years following the pandemic, the number of solutions aimed at mitigating the impact is ever-growing. Artificial Intelligence (AI) has long been considered a cornerstone of the approach by medical imaging vendors to tackle workforce shortages through workflow solutions, time-saving technologies and increasing scan readability. However, we are now, more than ever, seeing the role of AI in supporting the workforce translate into hardware trends. Patient-positioning cameras, motion sensors, and smart displays are just a few of the physical manifestations of the rising role that AI is playing in supporting radiologists in their operation of CT systems. This is allowing more junior radiologists to conduct more complex scans, sooner in their development, complete scans more quickly, efficiently, and accurately. It also reduces the need for rescans or extended support from more experienced radiologists. In response to the rise in demand for AI solutions that support stretched workforces, CT systems now have more Graphics Processing Units than ever before, to increase AI capabilities and the machine’s processing power.

The ongoing challenge of workforce shortages has paved the way for increased interest in remote scanning solutions. Remote scanning can help improve radiologists’ flexibility and enhance collaboration and training of more junior radiologists by harnessing the expertise of more experienced personnel who may not be in close physical proximity. There are still multiple barriers that risk the wider adoption of this technology, which include similar cultural and regulatory challenges that AI has seen in its rise. The financial, technical and infrastructure demands with such technology relying on robust cloud platforms, secure data-sharing systems, and more modern CT systems could also hinder its adoption.

Photon-Counting CT (PCCT) Continues Its Wave of Interest

Following on from the launch of Siemens Healthineers’ fleet of PCCT solutions at varying price points, the technology is now in reach to more settings than ever before. Subsequently, interest in its capabilities continues to march forward. As new, tailored applications for the technology emerge, the case for the financial viability of a PCCT system will grow over concerns that PCCTs will be used as conventional CTs more often than not. It is hard to ignore the anticipation of new market entrants into the PCCT market with many major vendors discussing their prototypes more and more candidly as time goes on. It is likely that a new entrant would focus on carving out its own niche either through hardware differences such as the detector itself, or through more specialised clinical applications such as oncology, neurology, musculoskeletal or specific low-dose applications.

Future Outlook

After the short-term dip, the CT equipment market is positioned for mid-single-digit growth in the next five years, as technology advancements continue to propel the modality’s capabilities forward in key clinical areas. The uncertainty in the US market will remain in the near term, as the impacts of the tariffs are realised. However, we project that the CT equipment market in China will return to stability, buoyed in the long term by favourable demographics, focused vendor investment and strong demand. New entrants to the PCCT market will be a step-change, with many anticipating a late-2025 launch bringing price competitiveness and novel approaches to the technology. As such, technological advancements will come back to the forefront, prioritised as an equal contender with price in purchasing decisions.

Related Research

CT Equipment – World – 2025

The fourth edition of Signify Research’s CT Equipment – World – 2025 report builds on its 2024 edition. It provides a data-centric and global outlook of the market. The report blends primary data collected from in-depth interviews with CT vendors to provide a balanced and objective view of the market.